Crude prices are fracking horrible – $100 billion is expected to be cut from the energy CAPEX (EIA).

Bullion.Directory precious metals analysis 9 February, 2015

Bullion.Directory precious metals analysis 9 February, 2015

By Christopher Lemieux

Senior Analyst at Bullion.Directory; Senior FX and Commodities Analyst at FX Analytics

Crude has had several “rallies” over the last two weeks, and is leading some traders to believe a bottom is being phased in. However, remember there were supposed to be several bottoms placed in at $80. $75, $70, $65, $55, and so on.

The total capitulation in the crude markets were the cause of horrendous fundamentals mixed with margin leverage, and it created a cocktail that will leave many with a headache.

The story is mixed. Bottoms are not formed simply because an asset is assumed to be oversold. Traders have been trying to catch the bottom in crude for months, only to be sliced and diced by falling knives.

The short-to-medium term data is still net-negative, and crude will likely meander between $45 to $55 per barrel until more definitive data pushes prices in either direction. A bottom in crude will be formed when a series of indicators and data show confluence.

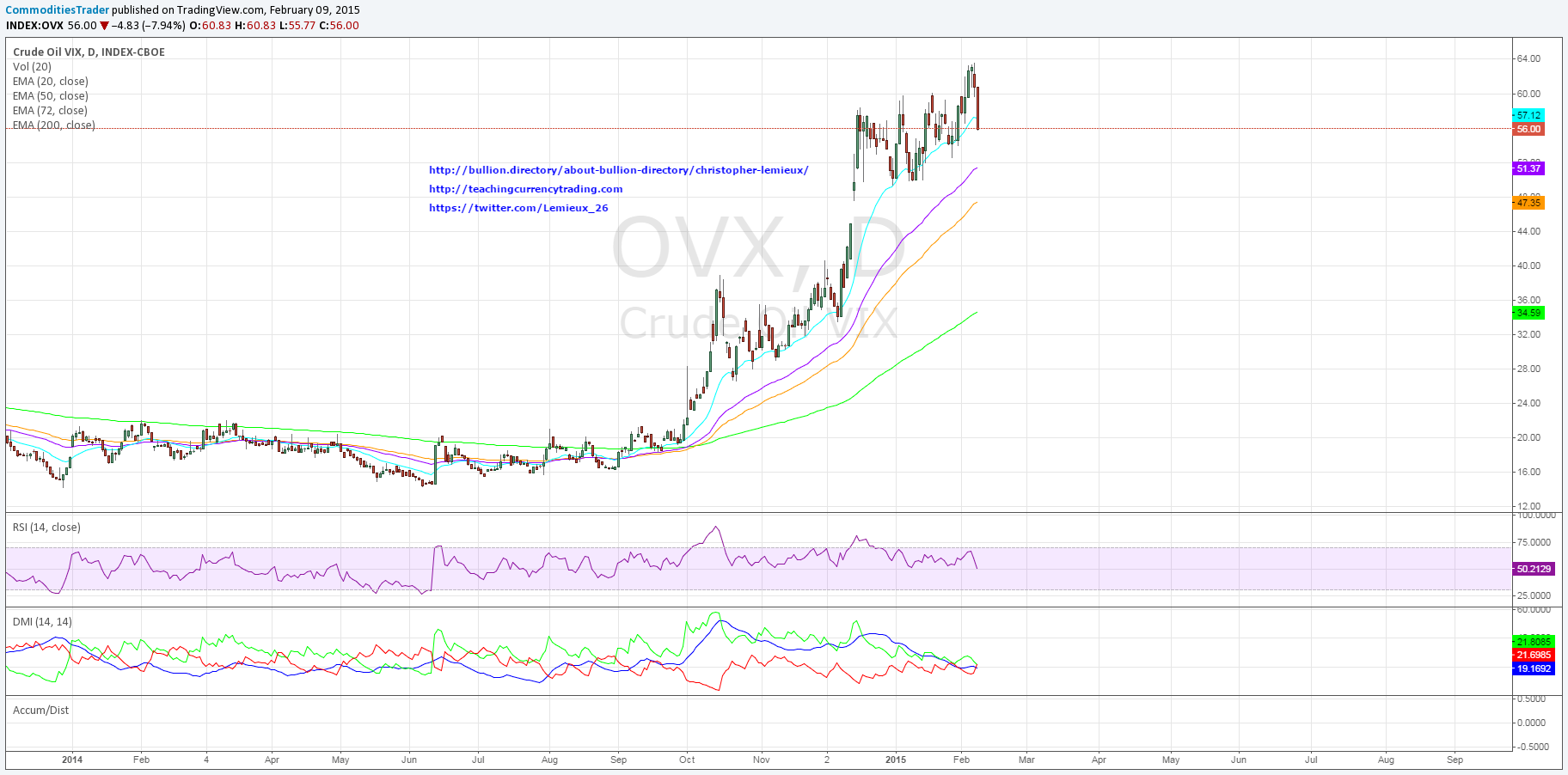

These mini-rallies are not too significant because, due to the increased volatility, crude is now a true trading vehicle.

Prior to the price’s utter collapse, crude was a large play among hedge funds. A lot like trends in equities, crude was bought on the dip, and prices always remained elevated.

Prior to last October, volatility remained low, if not just consistent. As volatility was ushered in, crude became a day trade to flip.

These rallies are largely made up of price-pumps going into the NYMEX close, and prices would crash moments after the market closed. Optiver – a proprietary trading firm based in the Netherlands – figured out ways to manipulate crude prices, while successfully doing so by trading a large number of contracts. This is not to say Optiver is the cause of these three, four, five percent daily gains in crude, but the price action is resembling day trading activity.

Notice the consistency in crude volatility, and then volatility became violent:

Fundamentals remain negative, too. An OPEC report suggested that oil demand would increase in 2015, and this gave traders something to feed on.

However, the gains were short-lived. The International Energy Agency (IEA) issued a report that supported the claim for increased demand next year, but the report added that crude stockpiles would continue to grow, especially in the US. Furthermore, the Energy Information Administration (EIA) said that even as demand could pick up, production will still out-pace demand by a few hundred-thousand barrels per day.

Vitrol Group, the world’s largest trader in oil, believes more downside could be around the corner.

CEO Ian Taylor said that even as oil companies are putting rigs offline, reaching multi-year lows, there are still no signs that US output is slowing down. Since January 14, the EIA crude inventories report showed a surplus of 30.7 million barrels. Taylor foresees the crude stockpiles to dramatically build over the next couple months before balancing itself out by the end of the year.

According to a report put out by Citi:

The recent rally in crude prices looks more like a head-fake than a sustainable turning point — The drop in US rig count, continuing cuts in upstream capex, the reading of technical charts, and investor short position-covering sustained the end-January 8.1% jump in Brent and 5.8% jump in WTI into the first week of February.

Short-term market factors are more bearish, pointing to more price pressure for the next couple of months and beyond — Not only is the market oversupplied, but the consequent inventory build looks likely to continue toward storage tank tops. As on-land storage fills and covers the carry of the monthly spreads at ~$0.75/bbl, the forward curve has to steepen to accommodate a monthly carry closer to $1.20, putting downward pressure on prompt prices. As floating storage reaches its limits, there should be downward price pressure to shut in production.

The oil market should bottom sometime between the end of Q1 and beginning of Q2 at a significantly lower price level in the $40 range — after which markets should start to balance, first with an end to inventory builds and later on with a period of sustained inventory draws. It’s impossible to call a bottom point, which could, as a result of oversupply and the economics of storage, fall well below $40 a barrel for WTI, perhaps as low as the $20 rage for a while.

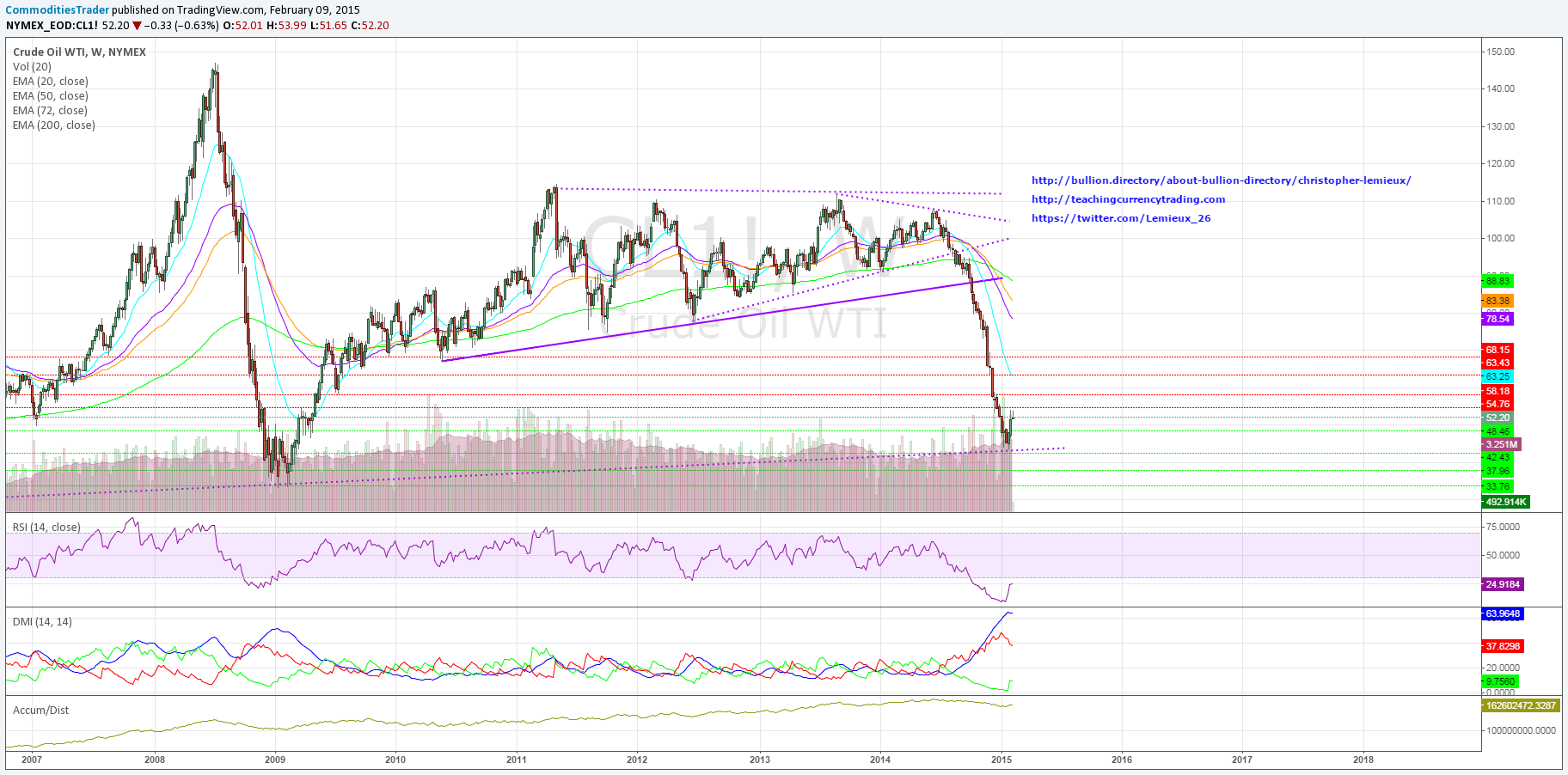

On a technical basis, crude prices simply caught up with deteriorating fundamentals. The leverage built into crude trading was the primary result of the steep, dramatic decline. As an energy trader for many years, crude began to catch my eye as it reached $80 per barrel, and I began to set up.

As seen here, I forecast that crude would drop a lot more as price action began to challenge a descending trend line that began at the apex of the crude bubble in 2008. If prices closed below this support level, selling would intensify – and it did!

I followed up with a chart that showed a more clearer picture, technically. To nearly every analyst I heard on the matter, crude was just on the precipice of bottoming around $50, but I felt that crude “wanted” to push lower.

Forecasting that crude would see $43.XX turned out to be spot on as West Texas Intermediate (WTI) dropped lower to $43.58 prior to seeing upside action:

WTI has played out fundamentally, and the fundamentals (along with sentiment) still remain to the downside. Traders love to pick out bottoms by catching falling knifes, and they’re usually cut up in the process.

On a risk:reward basis, sure WTI may seem like it’s at a nice area to buy. Yet, I think it is still to early. Crude will likely find support at the longer-dated support in the low $43’s per barrel. While I wouldn’t suggest opening fresh shorts without a pullback, it still may be early to gobble crude futures.

The implications are still apparent. Supplies are still gluttonous, and shale companies are hurting. WBH Energy has become the first casualty of the asymmetical oil warfare. I expect more to come, particularly Cheniere (idea to come).

I have been short since $74, and I wouldn’t suggest serious upside unless $53.5 is retaken.

Now, $53.50 has been seen a few times, but crude prices have not been able to build upon this. These “rallies” are almost always faded, and this could signal a lack of conviction to the upside. However, if crude prices can remain in range mode, a series of positive (or, maybe, slightly less bearish) inventory reports could help crude build a stronger bull case.

The only problem I see halting the mid-to-end of the year projections for higher crude prices is the global slowdown and dis-inflationary environment.

Growth has been lacking, and it is concerning that China – the largest consumer of oil – is showing real signs of trouble. GDP recently hit two decade lows, and the most recent import/export data is troubling. China saw a 3.3 percent decline in exports and a whopping 19.9 percent decline in imports YoY, the worst since 2009. It was was 16 percent lower than the general consensus.

There is also disinflation. Whether it is in the US, Eurozone, or China, prices for commodities will remain low. Crude is no exception.

A bottom in crude will not likely begin until fundamentals mingle with price action. Inventory builds of 5, 6, 10 million barrels per week will not help the case for higher prices, and oil companies could be forced to further slash rigs, jobs and CAPEX.

And considering the deteriorating economic data, more so in the US, 2008’s low could be retested.

Bullion.Directory or anyone involved with Bullion.Directory will not accept any liability for loss or damage as a result of reliance on the information including data, quotes, charts and buy/sell signals contained within this website. Please be fully informed regarding the risks and costs associated with trading in precious metals. Bullion.Directory advises you to always consult with a qualified and registered specialist advisor before investing in precious metals.

Leave a Reply